"Banking armageddon coming soon"

"Banks facing Challenges and Uncertainty"

The Grim Outlook for U.S. Banks: Implications and Challenges

- D23")

The outlook for U.S. banks appears grim as unrealized losses have surged by eight percent, equivalent to a staggering $42.9 billion. In this discussion, we will delve into the implications of this situation, particularly within the treasury market, and assess its significance for the broader banking sector. It is worth noting that even a minor bank failure could trigger a domino effect, leading to financial contagion. Regrettably, this issue has remained unresolved since March when several prominent regional banks faced insolvency. The Federal Reserve has diligently assisted through its BTFP (Bank Term Funding Program), but challenges persist.

Banking Challenges

FDIC data, which extended until the third quarter of 2022, revealed concerning losses. John warned against concentrating funds in a single bank, advising viewers to diversify their holdings, given his belief that a significant crisis loomed. Subsequently, the regional and U.S. banking sectors faced mounting pressure, necessitating rule changes by the U.S. Treasury to protect depositors holding amounts exceeding the insured limit of $250,000. Janet Yellen's testimony before Congress only heightened uncertainty when questioned about potential bailouts for small banks. Her response indicated that decisions would be made on a case-by-case basis, leaving the banking sector's fate precarious.

Considering the backdrop of rising inflation, bank failures, and extensive layoffs across various industries, the economic future remains uncertain. It is no surprise that central banks have been shoring up their gold reserves in preparation for what lies ahead.

The Bond Market Challenge

The primary reason behind the unfolding situation lies in the recent surge in interest rates and bond yields. This surge began when the Federal Reserve initiated its rate hikes, although the exact start date eludes me, possibly late in 2021 or early 2022. The rate increases were substantial and sustained for a significant period. Currently, they appear to have paused, with rate adjustments not occurring at every meeting, thereby calming the markets somewhat. However, the bond markets have continued to experience declines in prices, causing yields to rise.

Many banks and investors initially believed that the bond market would maintain its bullish trend, which had persisted since 1981. In 2020, some even purchased 10-year treasuries at yields below one percent. Fast forward to today, and these same securities now yield over four percent. This shift in yields has led to a decrease in the value of fixed-income investments in the secondary market.

The FDIC report for the second quarter released on September 7th, shows unrealized losses on securities increased substantially quarter over quarter. Unrealized losses on securities reached $558.4 billion in the second quarter, marking a rise of $42.9 billion, or 8.3 percent, compared to the previous quarter. Specifically, unrealized losses on held-to-maturity securities totaled $309.6 billion, while those on available-for-sale securities amounted to $248.9 billion.

Now, you might be wondering about the difference between held-to-maturity and available-for-sale securities. Banking regulations, as overseen by the FDIC, permit banks to value their securities at the purchase price for held-to-maturity securities. This approach assumes that if a bond, such as a treasury or mortgage bond, is bought at $100, it will eventually mature at that value, even if its market price temporarily drops. Available-for-sale securities are those that banks cannot categorize as held-to-maturity. For a more in-depth analysis of this topic, I recommend reading an article by Wolf Street, published on Friday, which provides valuable insights into the significance of unrealized losses on securities held by banks.

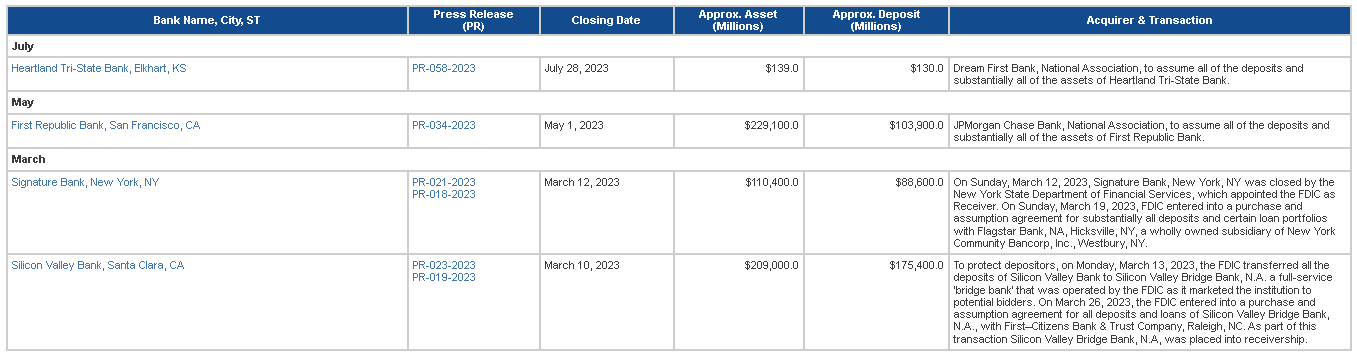

Investors and depositors have become increasingly aware of these unrealized losses. Notably, recent withdrawals from banks such as Silicon Valley Bank, Silvergate, Signature Bank, and First Republic reflect concerns regarding whether sufficient cash reserves would be available if more depositors followed suit. The U.S. banking sector is under considerable strain, with empty vaults and a shortage of physical cash.

Bond Yields and Their Impact

In summary, rising bond yields pose challenges for both the banking sector and the currency market, as treasury securities underpin the currency's value. Additionally, foreign entities are reducing their holdings of U.S. treasuries, aiming to replace dollars with their own currencies through initiatives like BRICS expansion. While some reports suggest robust foreign demand for U.S. treasuries, it's crucial to note that much of this demand comes from U.S.-domiciled offshore hedge funds, rather than traditional foreign entities. Nations like Saudi Arabia, Poland, Singapore, and China have been steadily accumulating gold as an alternative to treasuries.

Now, let's delve into why closely monitoring U.S. Treasury yields is vital, particularly in relation to the banking sector. For further insight, I'll share the FDIC report on unrealized gains and losses on investment securities. This report, as you can see, indicates improvements from the third quarter, with unrealized losses on held-to-maturity and available-for-sale securities decreasing. However, this improvement partly stems from realized losses being absorbed due to bank failures in March.

In essence, the blue portion represents held-to-maturity securities, while the beige segment comprises available-for-sale securities.

To better understand the implications of rising bond yields, let's consider a hypothetical scenario. Suppose on Monday, the U.S. Treasury issues a new 10-year note at par with a coupon rate of 4.25%. You purchase this bond for $100. However, three months later, the secondary market yield rose to 5%. If you decide to sell your bond, your bond dealer will offer a price lower than the initial $100 purchase price.

The decline in bond prices translates to a situation where selling your bonds would result in realized losses. This occurs because, with rising yields in the secondary market, the older bonds must be priced lower to match the new, higher yields. In essence, if you were to attempt to sell a bond for its initial purchase price of $100 while the market is offering a yield of five percent, no buyer would be willing to pay the full $100 because they would only receive a coupon rate of four and a quarter percent. Therefore, it is crucial to monitor bond yields, especially for banks, as they are obligated by regulations, both in the U.S. and elsewhere, to invest in government bonds, even though these bonds have recently proven to be far from risk-free.

A Closer Look at Bond Maturities

To provide a comprehensive view of the situation, I will analyze a range of bond maturities. Let's start with the two-year note. In the second quarter, the two-year note closed at a yield of 4.9 percent. Currently, the yield is almost five percent, resulting in a 10-basis point rise and potential losses for holders.

Moving to the five-year note, in the second quarter, it closed at a yield of approximately 4.16 percent. Presently, the yield stands at 4.4 percent, marking a 24-basis point increase since the end of June. This also leads to losses for those holding five-year notes.

Next, let's examine the ten-year note, one of the most closely monitored maturities. On June 30th, the yield was at 3.84 percent. Currently, it has climbed to 4.26 percent, representing a 42-basis point increase and potential losses for ten-year note holders.

Lastly, let's consider the 30-year bond. At the end of June, the yield was 3.9 percent. Today, it stands at 4.33 percent, reflecting a 43-basis point rise and potential losses for those holding 30-year bonds.

The situation has prompted the Federal Reserve to employ liquidity and credit facilities, such as the Bank Term Funding Program, to assist banks. This program essentially allows banks to exchange their depreciated treasuries for their original purchase price, even though the market values them lower. It's an unconventional move aimed at bolstering banks' balance sheets.

Furthermore, I've come across an article from The Wall Street Journal, dated September 8th, discussing the challenges faced by a small bank called Republic First. Unlike larger banks like First Republic, Republic First's customers have remained loyal despite its troubled balance sheet. However, this bank has raised concerns due to approximately 60 percent of its depositors being uninsured, meaning they hold more than $250,000 in deposits. If regulators were to close the bank without a takeover plan in place, uninsured depositors could incur significant losses. Such a failure could potentially trigger runs on other banks, leading to a broader contagion effect.

The Broader Implications

This situation highlights the possibility that even smaller banks' failures may be perceived as systemic risks by regulators. Although Republic First is only 0.2 percent the size of JP Morgan in terms of total assets, regulators are now considering the risk of contagion stemming from even smaller bank failures. The proportion of uninsured depositors in the U.S. banking system peaked in 2021, reaching its highest level since 1949, and only slightly decreased in 2022, according to the FDIC.

https://www.fdic.gov/bank/historical/bank/bfb2023.html

With over four and a half thousand banks in the United States, Republic First's situation could potentially be just the beginning of a more significant issue. There might be numerous other banks facing similar challenges under the surface. Some investors are attempting to stabilize the bank's situation. A shareholder group with a stake just shy of 10 percent announced exploratory discussions regarding an equity investment and a broader capital-raising deal with Republic First and potentially other banks. While the specifics of these discussions remain undisclosed, regulators are likely hoping for Republic First's survival. Even a relatively small bank could serve as the initial domino that sets off a broader crisis.

A Hedge Against Financial Instability

These developments underline the importance of holding some physical gold and silver in your possession as a hedge against financial instability. As the situation evolves, it becomes increasingly crucial to closely monitor U.S. Treasury yields and consider whether similar challenges are emerging in other regions, such as the UK and the EU. If a crisis unfolds in the U.S., it could have ripple effects throughout the global financial system. Additionally, the apparent breakdown in international cooperation and the shifting dynamics within the G20 add to the uncertainty. Observers around the world are undoubtedly keeping a keen eye on the evolving banking situation and its potential implications for the international order.

Conclusion

In the face of a potential Armageddon looming over the U.S. banking sector, it is evident that a storm is brewing, with implications that extend far beyond the financial industry. The surge in unrealized losses, driven by rising interest rates and bond yields, has cast a shadow of uncertainty over banks, investors, and depositors alike.

As we've explored the impact of these challenges, it's clear that even minor bank failures can have far-reaching consequences, potentially triggering a domino effect and financial contagion. The situation has prompted regulators to reassess the risk posed by smaller banks, underlining the need for a robust and flexible regulatory framework to safeguard the stability of the entire financial system.

Furthermore, the interconnectedness of global markets means that what happens in the U.S. banking sector reverberates worldwide. Foreign entities are reducing their holdings of U.S. treasuries, and nations are diversifying their reserves, seeking alternatives to traditional financial instruments. This shift has the potential to reshape the international financial landscape and impact the value of currencies.

In this uncertain environment, one thing remains clear: prudent risk management and diversification of assets are crucial for individuals and institutions alike. The lessons from the recent challenges faced by banks emphasize the importance of closely monitoring market trends, particularly in bond yields, and considering alternative hedges against financial instability, such as physical gold and silver.

As the banking sector navigates these turbulent waters, it is a reminder that vigilance, adaptability, and global cooperation are essential in addressing the challenges of our interconnected financial world. The future holds both uncertainty and opportunity and how we respond to these challenges will shape the path forward for the financial industry and the broader global economy.

Like, Subscribe, and Share to Spread the Word!

If you found this analysis informative and eye-opening, we invite you to like, subscribe, and share this video to help us spread the word. Together, we can build a community of Financial Anarchy advocates who are dedicated to promoting financial literacy and advocating for sound monetary policies. By amplifying our message, we can empower individuals to take control of their financial well-being and contribute to a more equitable and sustainable future.

Support Our Work with a Bitcoin Donation

We also offer the opportunity to support our work and help us continue building the Financial Anarchy community. If you would like to make a contribution, we gratefully accept donations in Bitcoin. Your support will enable us to create more educational content, engage in meaningful activism, and further our mission of challenging the status quo. To donate, please use the following Bitcoin address:

1EkmtWDYzuhkiv3iYozKVnZFxsQxDetnfH

Thank you for joining us on this journey of understanding and change. Together, we can shape a brighter financial future for all.