The Fall of the Final Pillar

Moody’s Downgrade and America’s Fiscal Reckoning

The Collapse of a 108-Year Legacy

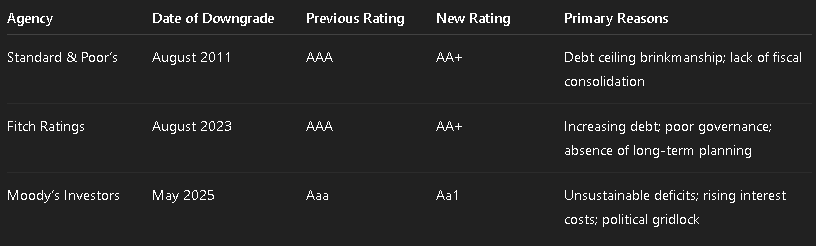

On May 16, 2025, Moody’s Investors Service downgraded the United States’ sovereign credit rating from Aaa to Aa1, ending more than a century of unbroken top-tier status. For the first time since World War I, the world’s largest economy no longer holds a triple-A rating from any major credit agency.

But this wasn’t just a change in classification—it was a judgment. The last pillar of American financial infallibility had been removed. Moody’s made clear: that the U.S. is no longer immune from the consequences of its own governance failures.

The agency cited a dangerous convergence: rising interest costs, unsustainable deficits, and entrenched political dysfunction. As of Q2 2025, the federal debt has surpassed $36.2 trillion, or 124% of GDP, while interest payments are projected to top $1.3 trillion annually, overtaking even military spending.

“The U.S. no longer exhibits the credit fundamentals consistent with a stable Aaa rating,” Moody’s wrote in its formal release.

The downgrade was not a sudden shock, but a public reckoning—a moment that crystallized what had long been building: the slow erosion of America’s fiscal credibility.

Market Repercussions: A Downgrade with a Price Tag

The market’s response was measured, but unmistakable. The downgrade did not trigger panic but it recalibrated expectations.

The Dow Jones fell 257 points on the morning of May 17.

The 30-year Treasury yield jumped to 5.08%, marking a 12-year high.

Mortgage rates climbed by 35 basis points, further squeezing housing affordability.

Gold reached $2,420/oz, as investors sought protection.

The dollar slipped modestly against major global currencies.

“This wasn’t about panic it was about repricing risk,” said Torsten Slok, chief economist at Apollo Global Management. “The U.S. is no longer perceived as risk-free. That’s a structural change.”

Even modest increases in interest rates can have massive fiscal consequences. The Brookings Institution estimates that each percentage point increase in borrowing costs could add $2 trillion in debt service costs over the next decade.

In short, this downgrade is an invisible tax—borne not just by governments, but by households, businesses, and future generations.

Political Gridlock and the Erosion of Fiscal Credibility

At the heart of Moody’s downgrade is not an economic crisis, but a political one.

The agency pointed to “persistent political dysfunction” as the defining feature of America’s fiscal decline. Year after year, Congress has failed to produce sustainable budgets, tackle entitlement reform, or pass lasting tax policies. Instead, it has lurched between short-term fixes and self-inflicted crises.

A Brief History of Dysfunction

2011: Debt ceiling brinkmanship brought the U.S. within hours of default. S&P downgraded the U.S. for the first time.

2013: Government shutdown over budget disputes paralyzed federal operations.

2023: Congress once again approached default before a last-minute deal.

Even well-intentioned efforts like the Simpson-Bowles Commission in 2010 were shelved casualties of partisan gridlock. Meanwhile, the 2017 tax cuts, extended in 2024 without offsets, added trillions in long-term obligations.

“The political system rewards delay and denial,” said Dr. Thomas Mann of the Brookings Institution. “Moody’s isn’t reacting to one event—it’s responding to a governing structure that no longer produces coherent fiscal policy.”

This is not a failure of one party or administration. It is a bipartisan failure to govern.

Rising Long-Term Debt Rates: Signals of a Global Debt Crisis

Low-yield environments are ending. With rising long-term yields, nations face increased refinancing costs, and debt-backed assets like property become significantly riskier.

Echoes from 2011: The Warning Washington Ignored

S&P’s 2011 downgrade was a watershed moment. It followed a bruising debt ceiling standoff and criticized the lack of a credible plan to stabilize long-term debt.

Markets reacted sharply, but the political system absorbed the shock without fundamental change. The years that followed brought budget showdowns, sequesters, and shutdowns but no structural reform.

“We hoped it would be a wake-up call,” said former Treasury Secretary Robert Rubin. “Instead, it became part of the background noise.”

That normalization of dysfunction set the stage for Moody’s decision fourteen years later.

Fitch’s 2023 Downgrade: The Second Strike

When Fitch downgraded the U.S. in 2023, it cited “fiscal deterioration,” “governance issues,” and a “lack of medium-term budget planning.”

The warning was clear but again, it was met with defensiveness rather than course correction.

“This should have prompted urgency,” said Maya MacGuineas, president of the Committee for a Responsible Federal Budget. “Instead, it was dismissed as technical noise.”

To international observers, the message was clear: the U.S. is no longer shielded by reputation alone.

Downgrade Timeline: A Decade of Declining Confidence

Global Fallout: A Shrinking Trust Premium

The downgrade has also widened cracks in the foundation of U.S. global financial leadership.

According to the IMF, the dollar’s share of global reserves has declined from 71% in 1999 to 58.3% in 2024. Meanwhile:

China’s digital yuan is gaining traction in regional trade.

BRICS nations are testing alternative payment systems.

Central banks have increased gold purchases for 11 consecutive quarters.

“This doesn’t mean the dollar is collapsing,” said economist Barry Eichengreen. “But the sense of inevitability the trust premium is eroding.”

No alternative yet rivals the dollar’s liquidity and legal protections. But trust is cumulative and its loss is incremental.

Looking Forward: Between Verdict and Recovery

The Moody’s downgrade is not a collapse—it is a verdict. A public accounting of years of fiscal mismanagement and political avoidance.

The implications are serious:

Higher interest costs will divert funds from public investments.

Federal programs face growing strain as debt service crowds the budget.

U.S. influence may weaken as financial leadership becomes conditional.

And yet, the story is not finished.

Reform is still possible:

A bipartisan fiscal commission with binding enforcement.

Entitlement adjustments through phased eligibility or means testing.

Tax code reform to broaden the base and eliminate corporate loopholes.

Debt triggers that automatically adjust fiscal policy when thresholds are breached.

“America hasn’t run out of options,” said Mohamed El-Erian. “But it has exhausted its ability to delay.”

Whether this becomes a turning point or a milestone on the path to further decline will depend not on markets but on leaders. The future of U.S. credibility is no longer guaranteed. It must be earned.

I would have thought the financial community would be upset about the number of electronic transfers from Treasure to customers of the financial institution being reduced would concern then…every wealth manager is fully aware of extraordinary transfers to particular customer of theirs.